The Fed just cut interest rates, but relief may be slow for struggling Americans as wealth inequality and inflation widen. Read the full analysis.

Table of Contents

The Fed Just Cut Rates. But Relief Might Not Come Quickly Enough for Some Americans

Introduction

The Federal Reserve delivered its first interest rate cut of the year, lowering its benchmark rate by a quarter point. While the move is aimed at easing borrowing costs and supporting households, the benefits may not reach all Americans equally. Consumer spending remains strong overall, but deeper analysis reveals a widening K-shaped economy — where wealthier households thrive while middle- and lower-income families continue to struggle.

A Strong Retail Picture Masks Inequality

Retail sales rose 0.6% in August, beating expectations and highlighting the resilience of consumer demand. But beneath this headline, a troubling divide is growing.

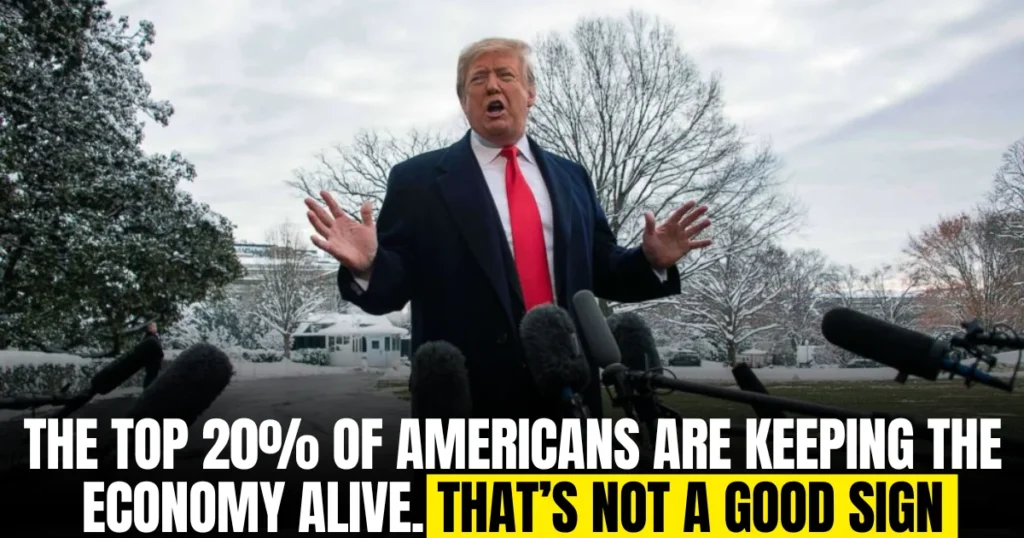

- The top 20% of earners now account for 63% of all US spending, the highest on record.

- The top 10% of households contribute nearly half of all spending.

- Meanwhile, many middle- and low-income families face tighter budgets due to inflation and higher borrowing costs.

Economists note that America’s growth is increasingly dependent on high-income households. If wealthy consumers begin to tighten their wallets — whether due to stock market volatility or declining confidence — the broader economy could quickly stumble into recession.

Rising Costs Hit Middle America

Inflationary pressures remain high, especially in services like travel, housing, and healthcare. Everyday Americans are adjusting in visible ways:

- Cutting back on leisure activities like concerts and fairs.

- Switching to discount retailers such as Walmart and dollar stores.

- Reducing food and grocery spending, even shifting to lower-cost chains.

For families like Scott Goodwin’s in Indiana, shifting to cheaper grocery stores is now a necessity, not a choice.

Tariffs, Debt, and Credit Stress

Former President Donald Trump’s tariffs on imports are further squeezing household budgets. Moody’s Analytics notes that while overall debt delinquencies remain stable, warning signs are emerging:

- Delinquency rates for households with sub-660 credit scores jumped to 9.06% in July, the highest since 2016.

- Meanwhile, new data shows that U.S. credit scores are slipping at their fastest rate in nearly 15 years, signaling rising financial stress for middle- and lower-income families.

- Wage growth for lower-income workers has slowed, reversing earlier pandemic-era gains.

These trends show that middle- and low-income families are carrying a heavier burden than wealthy households.

Why the Fed’s Move May Fall Short

The Fed’s quarter-point rate cut will lower borrowing costs slightly, but experts caution the relief will be uneven:

- Affluent households continue to spend freely, driving inflation in services.

- Lower-income families may see only marginal relief on credit card or mortgage refinancing.

- With inequality widening, overall consumer demand could weaken — putting long-term economic stability at risk.

KPMG chief economist Diane Swonk notes: “Inequality dampens overall spending. Lower- and middle-income households spend more of every dollar they earn, so when they’re squeezed, growth suffers.”

FAQs

Q1. Why did the Federal Reserve cut interest rates?

The Fed cut rates to ease borrowing costs, stimulate consumer demand, and counter slowing growth and rising financial stress among households.

Q2. Who benefits the most from the Fed’s rate cut?

Wealthier households and businesses with larger loans may benefit sooner, while lower-income families may see only modest relief on credit card and mortgage payments.

Q3. What is a “K-shaped economy”?

A K-shaped economy describes a recovery where wealthier households and corporations thrive, while middle- and lower-income groups face financial strain or decline.

Q4. How are tariffs affecting consumers?

Tariffs act like a consumption tax, raising the price of everyday goods. This disproportionately impacts low- and middle-income families who spend more of their income on essentials.

Q5. Will rate cuts stop a potential recession?

Not immediately. Monetary policy takes time to filter through the economy, and with inequality widening, rate cuts alone may not be enough to prevent a downturn.

Conclusion

The Fed’s decision to cut rates is a step toward easing financial pressures, but it doesn’t address the widening inequality at the heart of America’s economy. With the top 20% of households driving growth while millions face tighter budgets, the relief may be too little, too late for struggling families.

For long-term stability, policymakers will need to confront the structural issues of inequality, wage stagnation, and rising living costs — challenges that no single rate cut can resolve.